Musings on (Public and Private) Markets - #1

(1) Thoughts on hedging strategy for VC funds, (2) Finding investing signals in the Colossus podcast series

Background

I am trialling out a new format called ‘Musings on (Public and Private) Markets’ with the objective of sharing (hopefully) interesting analyses/thoughts on tech investing. These are not fully-fledged concepts/ideas, but rather initial thoughts. I hope to use this format as a way to interact with people that read the post and further develop these ideas. Please feel free to reach out to me via Twitter or by replying to this email if you would like to share your views.

Today’s post will comprise two different ideas:

Thoughts on hedging strategy for VC funds

Finding investing signals in Patrick O’Shaughnessy’s Invest Like the Best / Colossus podcast

1. Thoughts on Hedging Strategy for VC Funds

IPOs are considered a key milestone not only for companies but also for VC investors as they can finally crystallize returns for their LPs by selling their stake in the publicly listed company.

In regard to disposal timing, the decision is primarily constrained by two different mechanics:

Post-IPO, existing investors are typically not allowed to sell their stake during the lock-up period (typically ranges from 90-180 days).

Most VC funds have some level of discretion on when to sell the stake post-lock-up expiry, but are “forced” to sell their investments before the end of the VC fund life cycle (typically 10+2 years).

Furthermore, the fund returns for a VC fund are typically very sensitive to the post-IPO performance of its “public portfolio”. Hence, GP’s decision when to sell is quite important.

Given these constraints and the importance of disposal, I wonder whether some funds end up in a situation where they are forced to sell during a market correction, such as the tech correction in May-21, or sector / factor rotation. While it is arguably an “edge” case, VC funds could potentially hedge by purchasing put options on the index (QQQ, Nasdaq, Russel 2000, others) as a tail risk insurance. [I have deliberately not suggested buying put options on the portfolio company itself due to potential regulatory issues and because it is “off-brand” for VCs]. Hedging obviously requires taking a view on capital markets, GPs can potentially de-risk the fund performance to some degree.

There are several structural reasons why the majority of VC funds don’t hedge. Firstly, is the hedge still attractive after accounting for its cost? Secondly, who should bear the cost of the hedge - LPs or GPs? Thirdly, the majority of VC funds may not have access to prime brokerage to purchase hedging instruments. Finally, VC funds typically do not have the in-house capital markets expertise.

However, I do think that not enough time and energy is spent on disposal timing and structuring relative to the importance of such a decision on fund performance. There is definitely something that can be done - just have to get a bit creative. ;)

2. Finding Signals in Podcasts

Patrick OShaughnessy’s Invest Like the Best / Colossus podcast series is one of my favourite podcast series and an amazing way to learn more about investing as well as businesses. Besides established investors, Patrick also interviews founders/CEOs of often publicly listed companies such as StitchFix, Shopify, Cloudflare etc. Furthermore, various experts conduct an extensive deep dive on various businesses on the Business Breakdown podcast series. You can browse all podcast episodes here.

Patrick’s podcast series mostly features best-in-class, founder-led businesses (mostly in tech) that have scaled successfully and are considered great platforms. Furthermore, these businesses have a lot of growth potential. I consider it a great source to screen for quality businesses and help narrow down companies I would consider investing in.

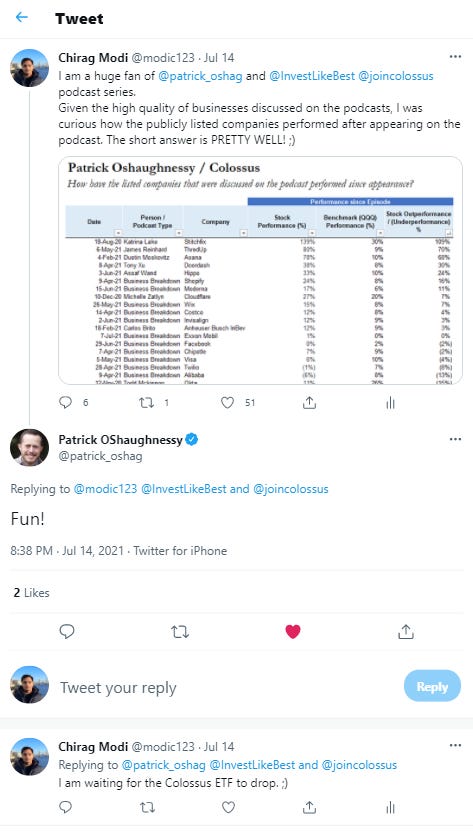

I was curious about how these publicly listed companies would perform relative to the market and did a quick and dirty analysis.

The table above (sorted by relative outperformance) shows the first time a company was featured on the podcast series and its share price performance since its appearance until today. Furthermore, the relative performance vs. benchmark index (I used QQQ) is shown in the last column.

The results are truly astounding. The majority of businesses have outperformed the QQQ benchmark, with StitchFix outperforming by a whopping 109% since Katrina Lake appeared on the podcast in Aug-20. On the other end, Pinduoduo, which appeared on the Business Breakdown podcast on 8-Jun-21, has underperformed by 20%.

This is obviously a “fun” analysis and the results are not conclusive due to the small sample size and other statistical considerations. However, I can’t help but wonder whether these companies will outperform in the long run. In any case, I did suggest that Patrick should launch a Colossus ETF. ;)

Disclaimer

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and affiliated persons and companies assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

The idea that a VC can hedge its fund's returns by buying a put option on a relevant index is interesting. Thanks for writing about this!