A Closer Look at Large-cap European Tech in Public Markets

71 tech companies with >€1bn market cap. Full list available on request.

There is a consensus that Europe has lagged behind the US and China in tech innovation due to a variety of reasons. Europe has been considered terrible at nurturing successful tech companies with only a few reaching significant scale (>€1bn value) compared to the US. While the debate has focused on private markets, much of the same negative sentiment / consensus is echoed in the European public markets with the tech sector to be “small” and overshadowed by the old economy.

In this post, I take a second look at the listed European tech sector to better understand its composition and assess its attractiveness from a long term investor’s perspective. I summarize my key initial findings in this post. Please reach out if you would like access to the data or exchange thoughts on this topic.

There are 71 tech companies with >€1bn Market cap in Europe

Based on my screening, there are 71 European tech companies with a market cap above €1 billion, representing an aggregate market cap of €1.1 trillion (as a reference, Apple’s current market cap is €1.9 trillion). It should be noted that there is a long tail of 250+ smaller companies (<€1 billion market cap) with an aggregate market value of €90+ billion.

Sector Distribution

Semis / hardware represent the largest segment. I was slightly surprised as it is not a sector I know well and hence was not aware of its scale. There are several large companies such as ASML, Infineon, STMElectronics in Europe. I suspect that the global nature of the semis, coupled with its manufacturing capabilities, enabled European companies to reach such scale.

Consumer Internet is the second largest segment and comprises dominant regional players in classifieds / platforms, food delivery and e-commerce. Whilst there are several new-age players, particularly in food delivery and ecommerce, low-tech classifieds (Adevinta, Scout24, Schibsted) still represent a large portion of this segment.

Software segment is the third largest segment with an aggregate market value of c. €235 billion (SAP represents c.60% of the aggregate market value).

Majority of the European software companies are “mature-tech” with revenue growth <10%. However, several promising, high-growth companies such as TeamViewer have recently IPOed and reached significantly scale.

It should be noted that successful high-growth tech companies tend to prefer a US listing (e.g. Spotify, Elastic), limiting the listing of break-out software companies in Europe.

Gaming is the third largest segment with 7 out of 10 companies listed in two geographies (Sweden and the UK). Selected companies include Ubisoft, Embracer Group, CD Projekt, Keywords Studios.

Others including (a) Edtech (Kahoot!, Learning Technologies), (b) HoldCo (Prosus), (c) Payments (Adyen) and (d) Ocado

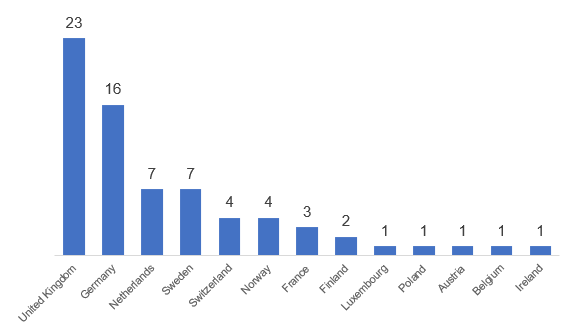

Geographic Distribution

As expected, the majority (61%) of the tech companies are HQed / listed in the UK, Germany and Netherlands, which are the largest and mature financial exchanges in Europe. I was quite surprised to see 13 companies listed on the Nordic exchanges, containing some hidden gems in the European tech universe.

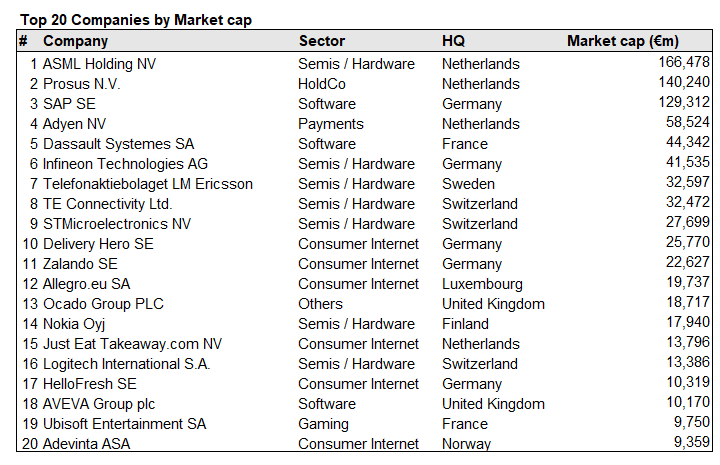

The 20 largest tech companies in Europe

The table above shows the top 20 largest listed tech companies in Europe, representing an aggregate market cap of €300 billion (c.27% of total universe). Some observations

Lack of European “FAANG” - There is a clear lack of tech majors in Europe. While the US have their FAANGs and China have their BAT stocks, Europe doesn’t have any tech companies of such scale. In fact, most investors won’t even be familiar with the largest European tech company - ASML, a leading manufacturers of chip-making equipment.

“Old-school” Semis / hardware are overweight on the list, similar to the overall sector distribution - As per the aggregate sector distribution, semis / hardware dominate the top 20.

Several new-age, consumer internet players dominating - One common theme within the consumer internet is the emergence of dominant regional platforms in various verticals (classifieds, ecommerce, food delivery). Companies such as DeliveryHero, Zalando and Allegro dominate multiple geographic markets, enabling them to reach significant scale.

Where are the software companies? There is a clear lack of software companies in the top 20. SAP, Dassault and AVEVA are the only software companies on the list. In contrast to the US, Europe is a tough place to scale a listed software business due to a variety of structural reasons (geographic fragmentation of end markets and smaller IT budgets relative to the US, investor focus on profitability etc).

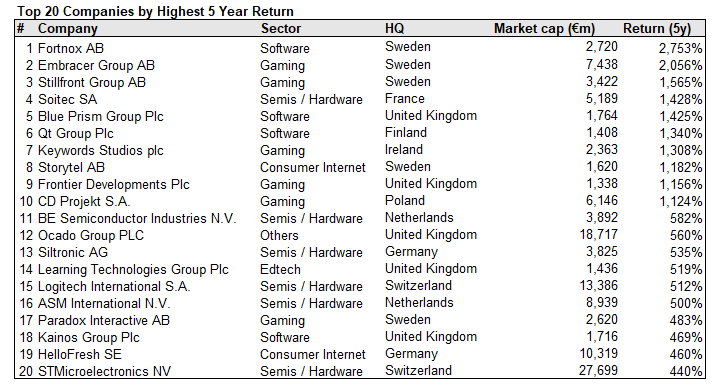

Highest Return over a 5 Year Period

The table above shows the highest total shareholder return (assuming dividends are reinvested if applicable) over the last 5 years. It is difficult to derive a common theme. While +10 baggers exist in every market, the relative small cap nature of these companies and geographic dispersion makes it more difficult for retail or institutional investors to identify these attractive opportunities.

Investing in European tech requires access to and knowledge of several local markets (UK, Germany, Nordics) and a holistic sector knowledge (semis, gaming, software) as opportunities are spread across sectors and geographies. Absent the ZIRP state of the world, an optimist would argue that the complexity would perhaps makes it a compelling playground for sophisticated European retail and institutional investors, wanting to generate alpha on home turf. However, as long as the US tech keeps hitting ATHs, investors don’t need to do the hard work in European tech.

Thanks for this Chirag, very good concise overview, appreciate it